Tesla (nasdaq: tsla)) did not launch exactly 2025 on a high note – the stock is down 36% with the first quarter now behind us.

All eyes are now turning to delivery numbers of the first quarter of the company, which should arrive this week – and the atmosphere is not exactly electric. Sales in January and February fell sharply in several key world markets – a subsidence of many attributes directly to the CEO Elon Musk, whose political activities have made him a non -grata character among potential consumers. As a result, several Wall Street analysts have revised their sales and downward delivery projections.

An investor, known by the pseudonym research of Bluesea, thinks that real figures could very well be even worse than many.

“I believe that we could see a drop in Yoy greater than expected of figures for the first quarter due to the negative deliveries of international regions,” predicts the investor.

Bluesea is particularly concerned that if Tesla is below 300,000 deliveries for the quarter – it is a drop from one year to the next of more than 20% – this could trigger another series of losses for shareholders already beaten.

In addition, the investor argues that those who hope for a robust Robotaxi update to save the day are intended for disappointment. Not only is the launch of this service only scheduled for June, but Bluesea also stresses that Tesla seems to be far behind the Waymo technology of Google, which openly tested the platform well before its sales service was born.

“Tesla has not shown a similar test phase for its Robotaxi service,” adds the investor. “Waymo has established a gold stallion in its service and Tesla should provide comparable service to gain customer confidence.”

Another strike against Tesla is the wide range of sales and benefits that analysts offer. For Bluesea, this inconsistency is not only noise – this underlines how uncertain short -term trajectory is.

“BPA eventually and income estimates vary considerably, which shows the massive risk associated with the stock while it is negotiated with more than 100 multiple PEs,” concludes Bluesea, who assesses TSLA shares a sale. (To look at the history of Bluesea Research, click here)

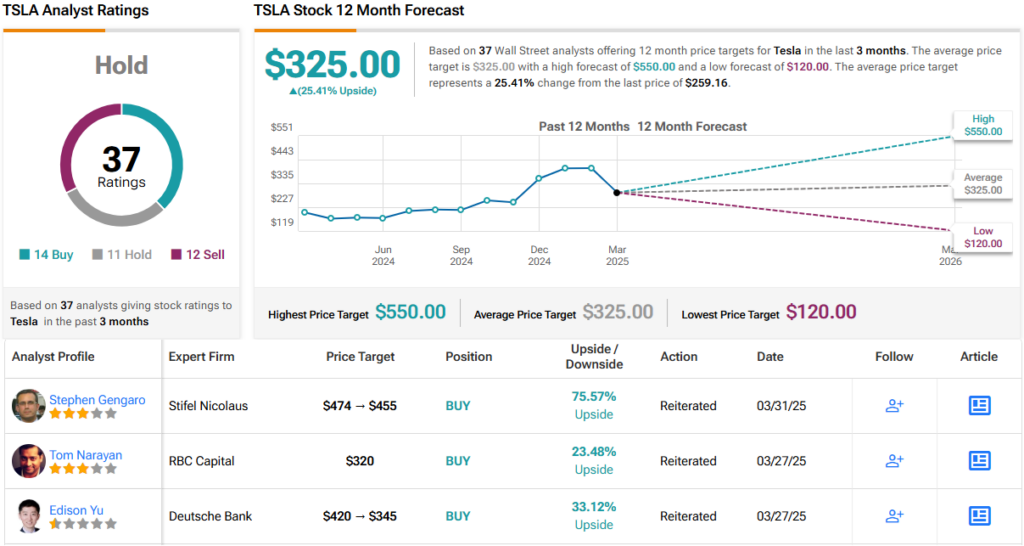

Meanwhile, Wall Street remains firmly on the fence when approaching the report of deliveries of the first quarter. The ventilation of consensus is almost divided, with 14 purchases, 11 sockets and 12 sales, adding to a lukewarm consensus (that is to say neutral). However, the average price target of 12 months of $ 325 suggests a potential advantage of 25% compared to current levels. (See Forecast of TSLA actions))

To find good ideas for negotiation actions to attractive assessments, visit the best Tipranks actions to buy, a tool that unites all information on Tipranks actions.

Warning: The opinions expressed in this article are only those of the star investor. Content is intended to be used for information only. It is very important to do your own analysis before investing.

Warning and disclosure