Adios, “Spring according to Season”.

By Wolf richter For Wolf Street.

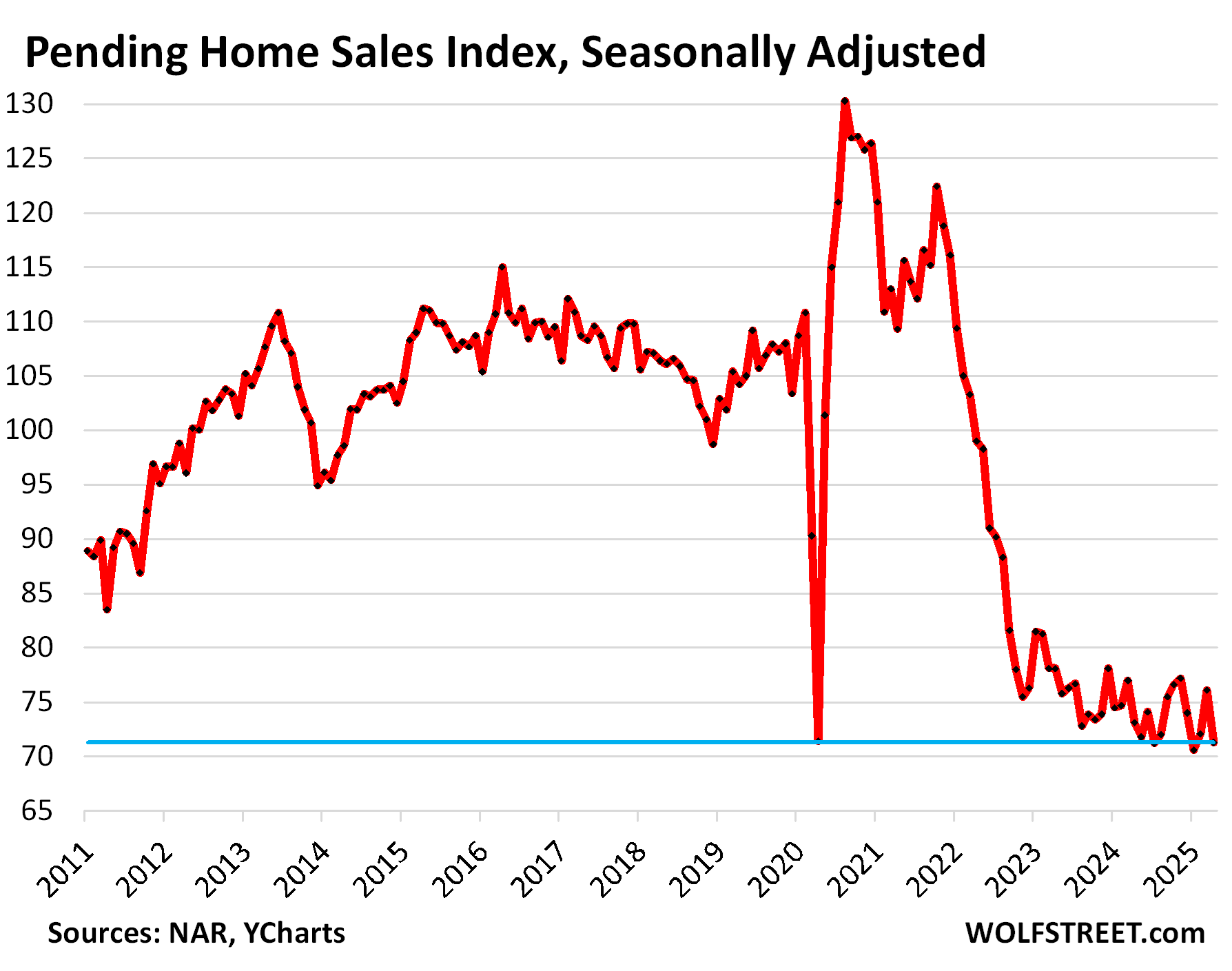

Sales of pending houses, an indicator shot forward of the “closed sales” of existing houses, plunged 6.3% in April from March, adjusted seasonally, according to data from the National Association of Realtors today, driven by dives even more important in the South and West, with the West by cutting up new stockings in the data, as well as the inventories to sell.

Compared to April in previous years (historical data via Ycharts):

- 2024: -2.5%

- 2023: -8.7%

- 2022: -28.0 %%

- 2021: -34.8%

- 2020: -0.1% (locking in April)

- 2019: -31.6%.

Pending sales reflect the contract signatures and follow -up offers that have not yet closed and which could still collapse or be canceled, for all kinds of reasons, such as buyers unable to afford or even obtain the owner’s insurance, or to finance. Although the signed contracts that undress later are included in waiting here, they are not included in the closed sales data reported later.

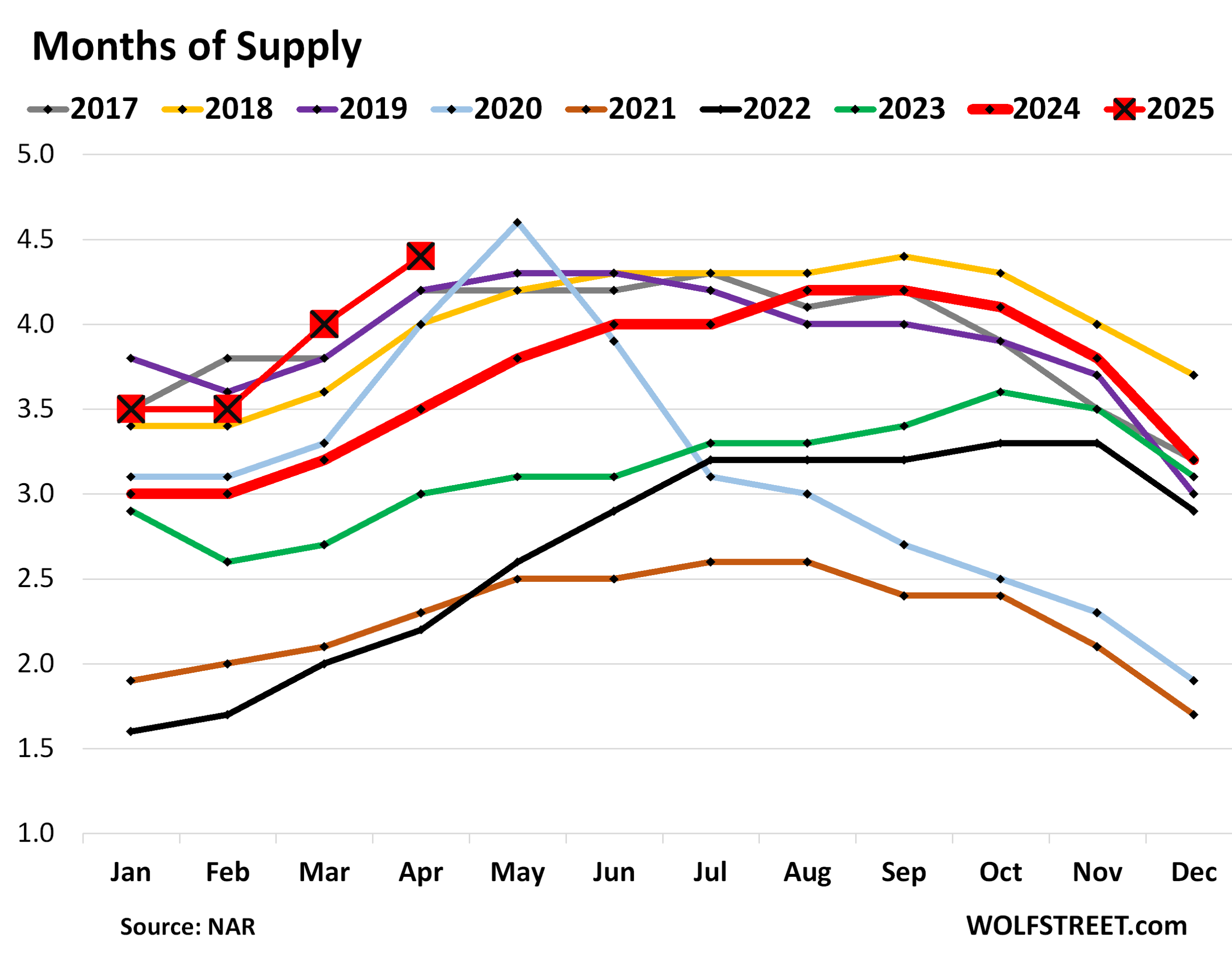

“In addition, with the inventory levels of housing reaching five years, house buyers in almost all regions of the country are better placed to negotiate more favorable conditions,” said the report.

Indeed. The prices of houses have increased by 50% in addition to a few years during the pandemic, and these artificially swollen prices of the sky triggered the destruction of demand on a massive scale, this is what we see here – one of the most fundamental economic principles. When retailers or airlines are struck by the destruction of demand, now measured in real time online, they instantly react by lowering prices and demand returns. The housing market is still struggling to understand that the lower prices, after the artificially supplied point, would revive demand.

The offer of houses for sale in the United States increased to 4.4 months in April, The highest for all April since 2016::

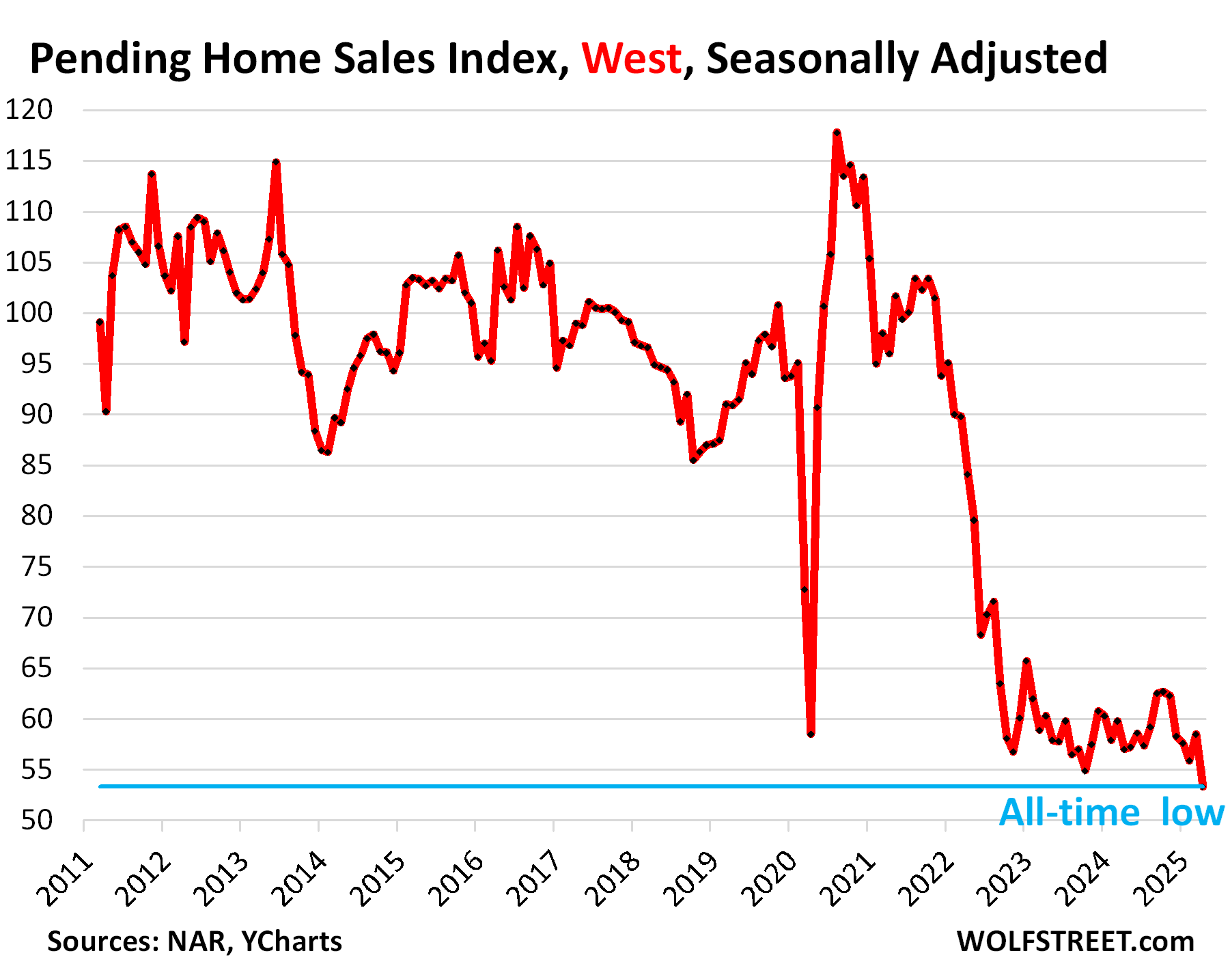

In the West: collapsed sales, balloon stocks.

Sales awaiting existing houses in the West (see the map of the four census regions in the comments below) plunged 8.9% in April from March, adjusted seasonally, at the lowest rate of data dating back to 2011.

Sales pending in April compared to April in previous years:

- 2024: -6.5%

- 2023: -11.6%

- 2022: -36.6%

- 2021: -44.5%

- 2020: -8.9% (locking in April)

- 2019: -41.4%.

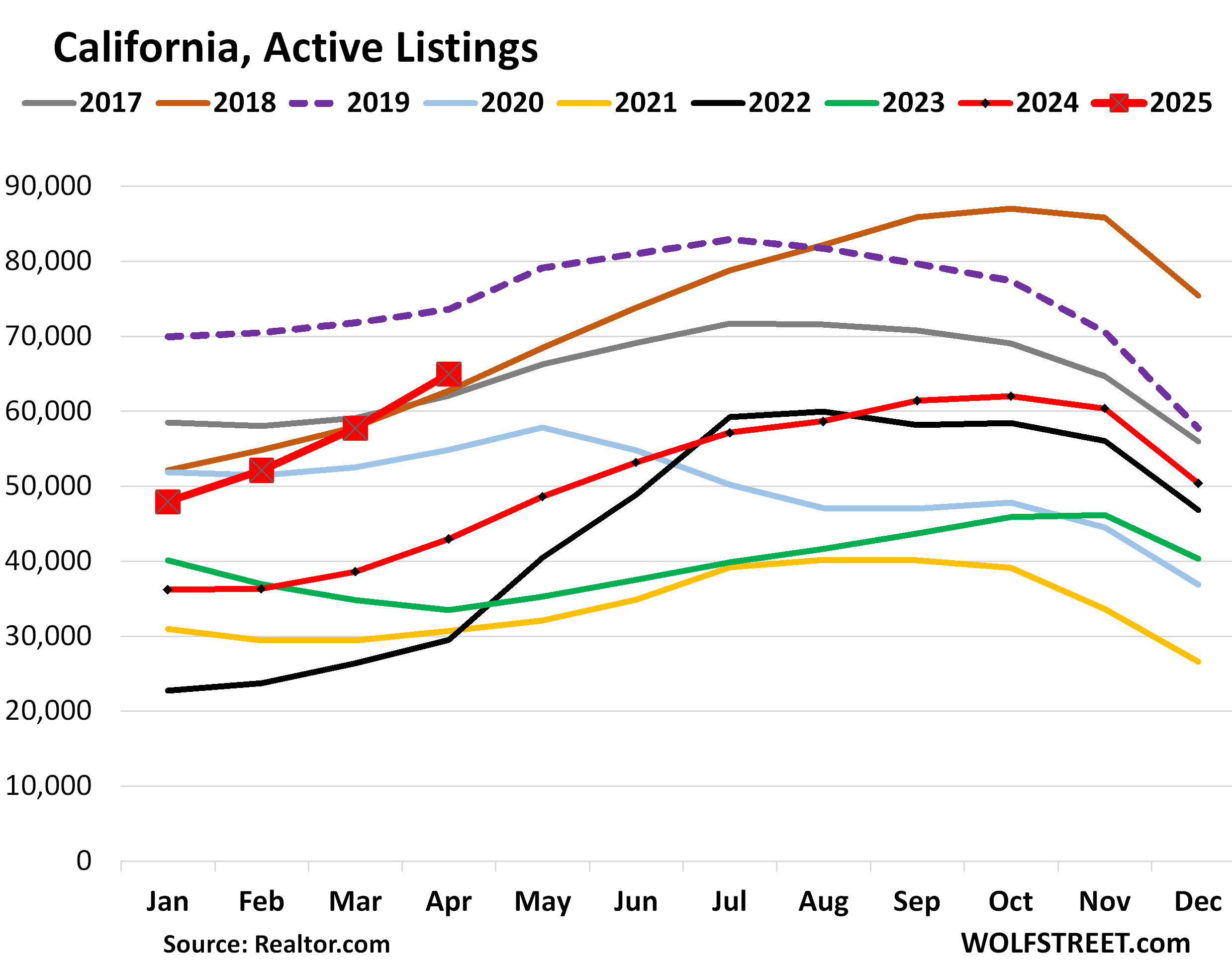

Inventory of existing houses In the West, are dominated by the huge California market. The active lists of existing houses in California increased by 51% in annual sliding in April, to 64,963 houses (red squares in the graph below), the highest for all April in data of data data data Realtor.com Let’s go back to 2016, except for 2019 (dotted purple line):

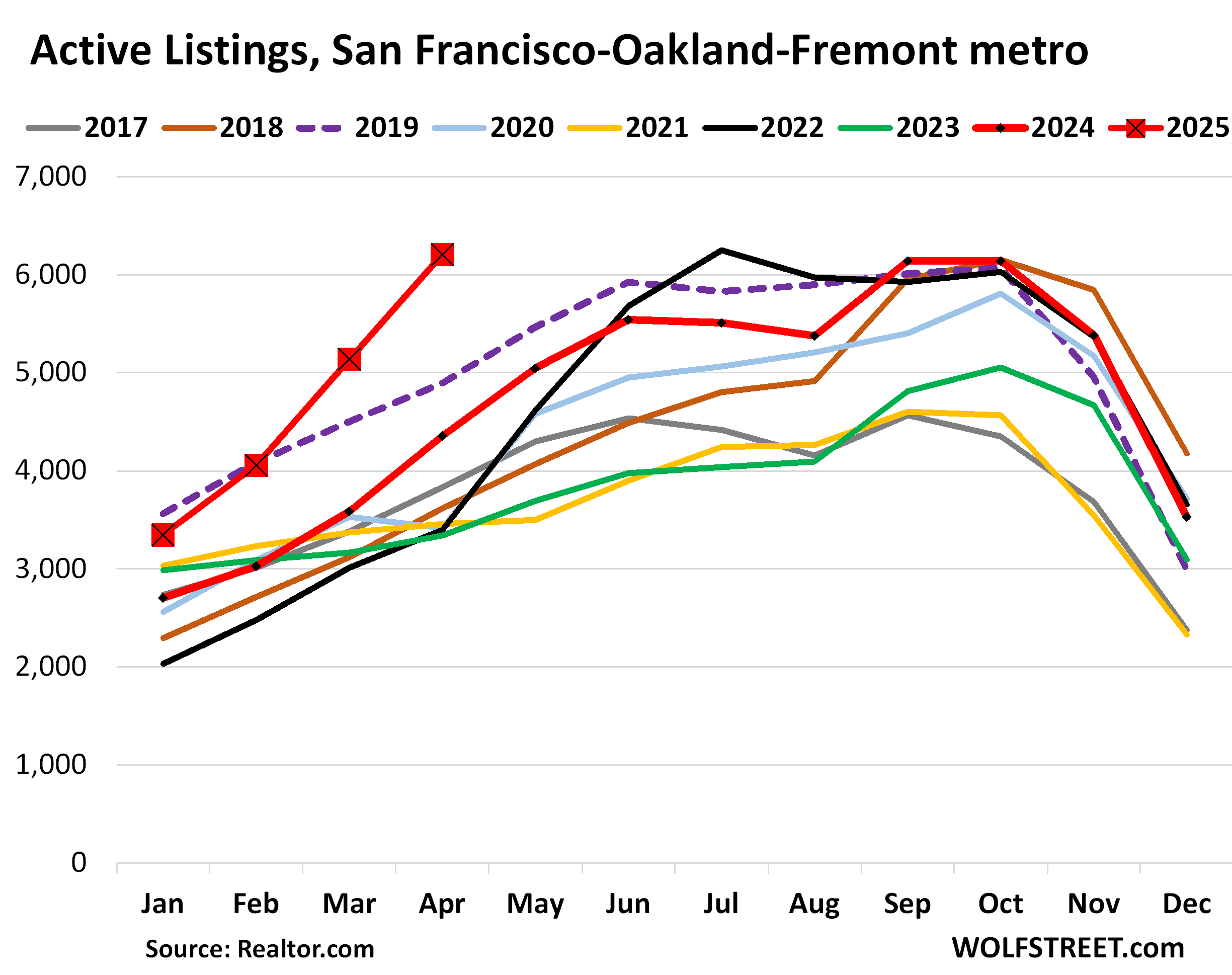

The balloon inventory for sale is a good thing for the too expensive American housing markets. This is what these markets need the most. So inventory is ping up in all major markets in California, Such as by +70% Year-over-Year in San Diego County, +68% in the San Jose-Sunnyvale-Santa Clara Metro, +50% in Los Angeles County, +43% in the Fresno Metro (Central Valley), +75% in Orange County The San Francisco-Oakland-Fremont Metro, where the accumulation of stocks is a little more advanced than on some of the other Californian markets (we discussed The main California markets here):

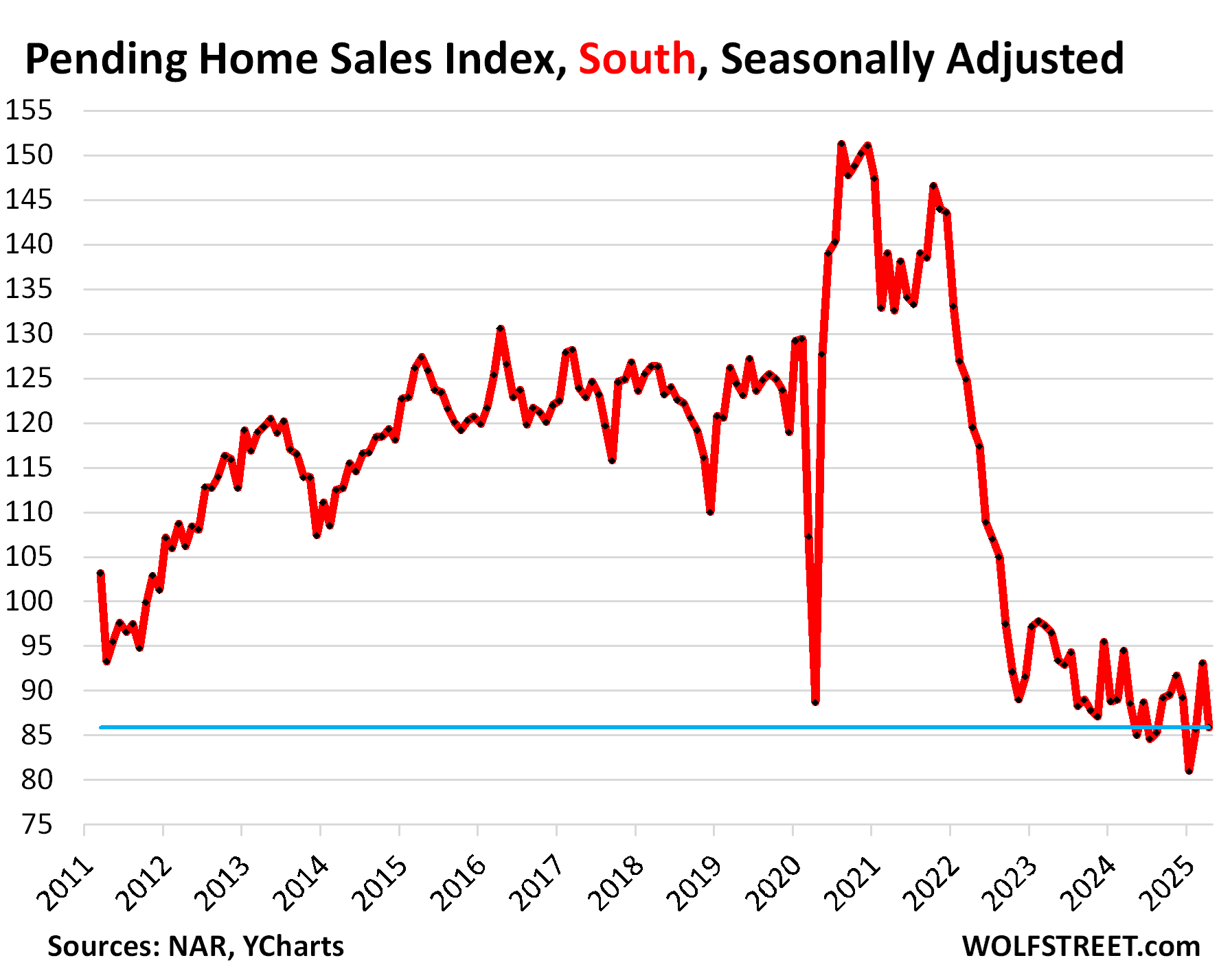

In the south: collapsed sales, balloon stocks.

Pending sales plunged 7.7% in April from March, seasonally adjusted, below locking in April and April worse, data.

Sales pending in April compared to April in previous years (historical data via Ycharts):

- 2024: -3.0%

- 2023: -11.0%

- 2022: -28.1%

- 2021: -35.2%

- 2020: -3.2% (locking in April)

- 2019: -30.9%.

It is precisely in the south where stocks accumulate.

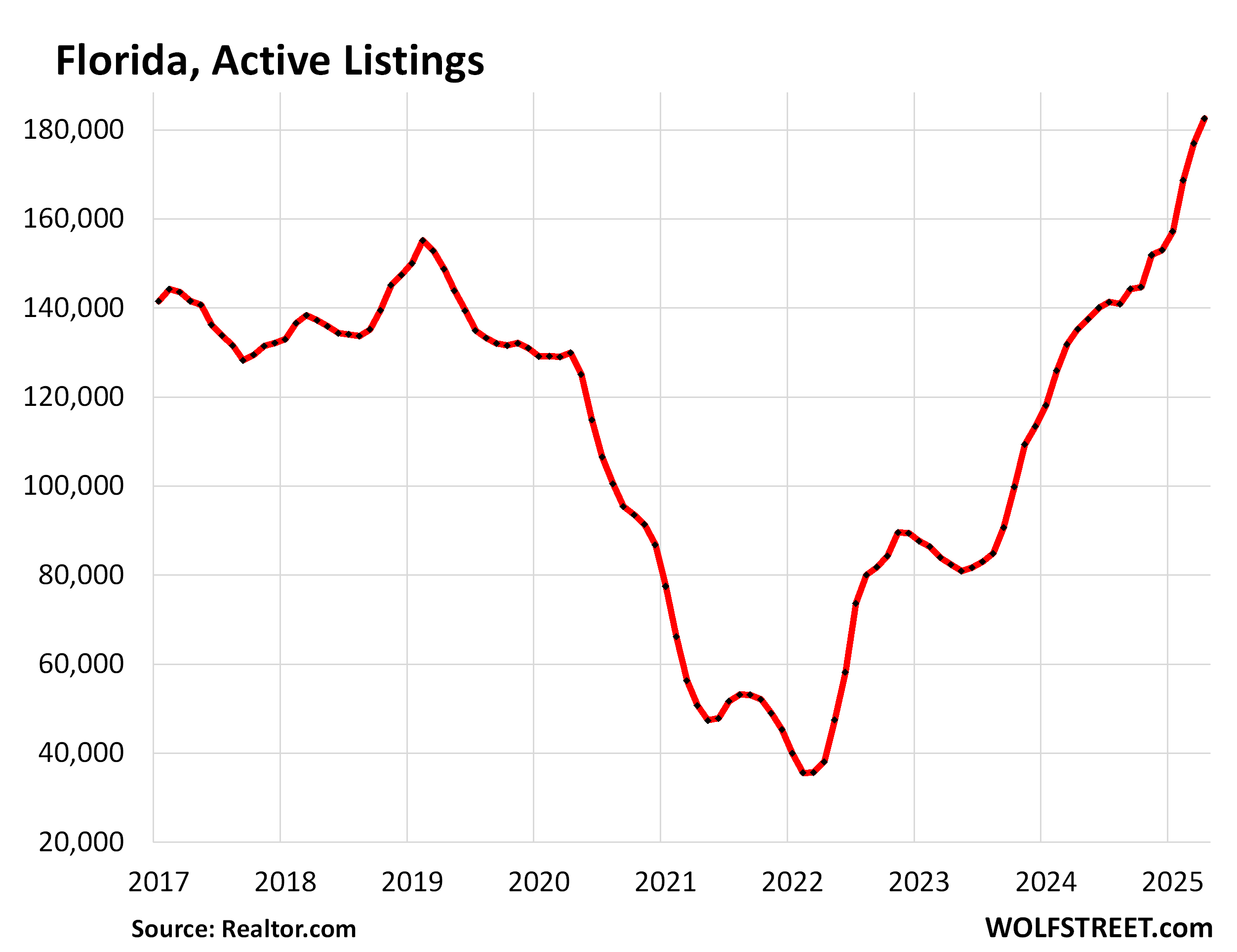

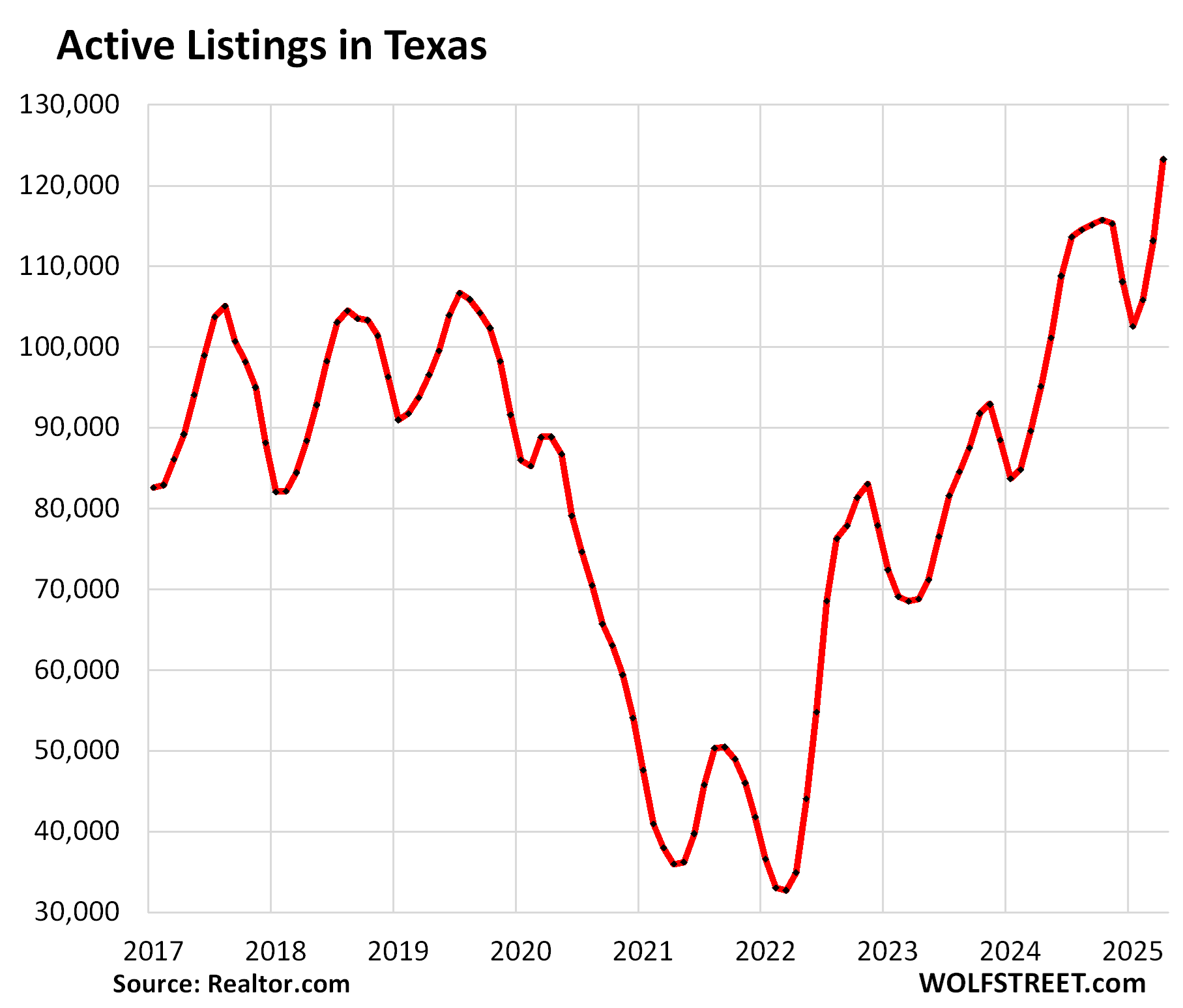

Florida and Texas dominate the vast south (map of the regions in the comments below). And this is where the stocks of existing houses are soaring, which is a good thing because the housing market needs these inventories.

In Florida, the active lists of existing houses increased by 35% In annual shift in April, at 182,589 lists, the highest data by Realtor.com Let’s go back to 2016.

In Texas, the active lists of existing houses jumped 29% In annual shift in April, at 123,237 lists, the most inventory of data from Realtor.com dating back to 2016.

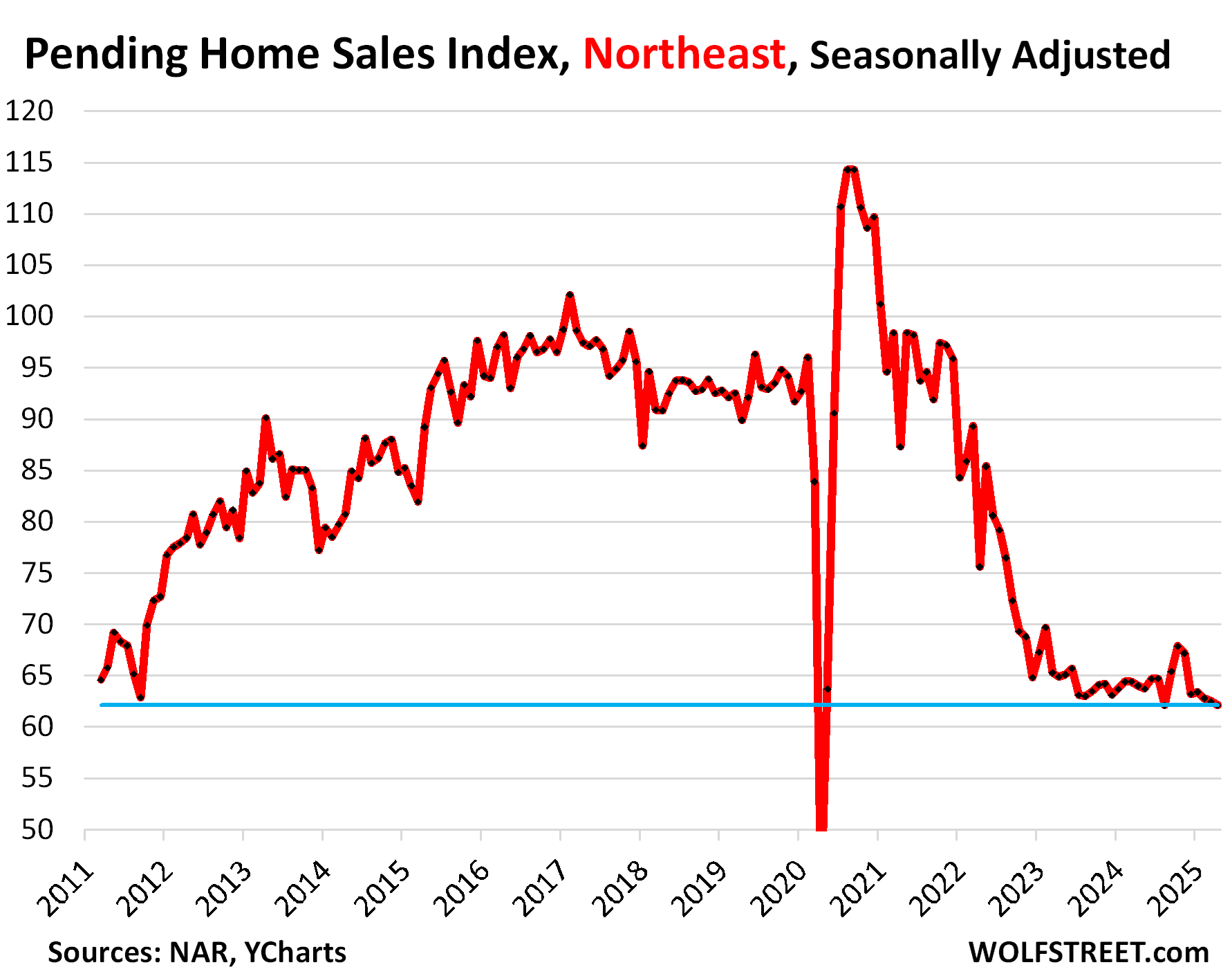

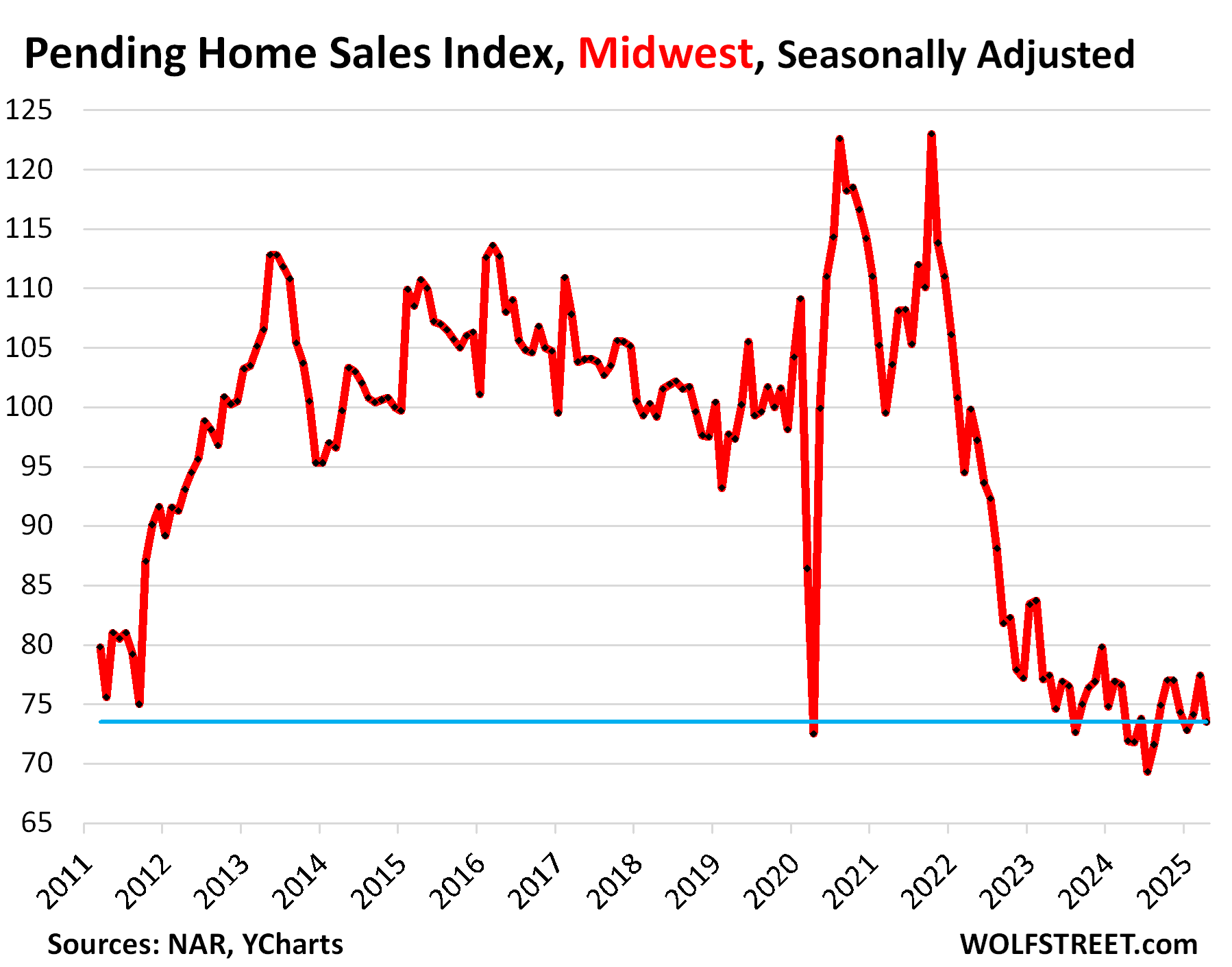

Sales in the northeast and midwest.

In the northeastSales awaiting existing houses dropped by 0.6% in April from March, seasonally adjusted, the worse April of the data, with the exception of the April 2020 locking, when sales have essentially dried.

Compared to April in previous years:

- 2024: -3.0%

- 2023: -4.3%

- 2022: -17.9%

- 2021: -28.9%

- 2020: + 43.1% (locking in April)

- 2019: -30.9%.

In the Midwest, Instructions have dropped 5.0% in April from March, seasonally adjusted, but increased by 2.2% from April 2024, and hair above locking in April 2020.

Compared to April in previous years:

- 2024: + 2.2%

- 2023: -5.0%

- 2022: -26.4%

- 2021: -29.1%

- 2020: + 1.4% (locking in April)

- 2019: -24.5%.

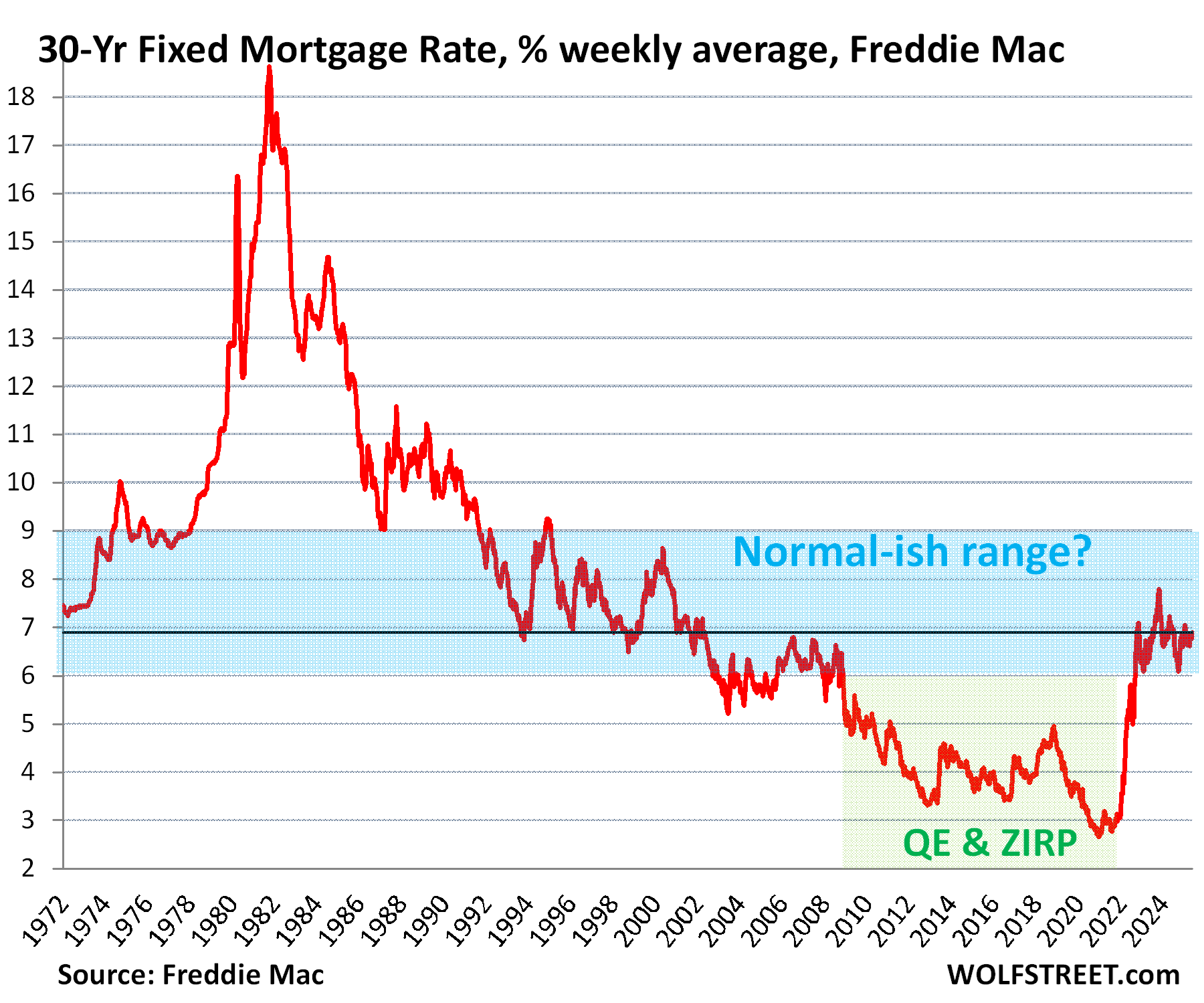

Mortgage rates are back in the normal range.

The average fixed mortgage rate of 30 years increased to 6.89% during the last week of report, according to Freddie Mac today. It has been more than 6% since September 2022.

Mortgage rates below 5% have been caused by the Fed QE, including the purchase of large amounts of securities backed by mortgage claims, associated with low inflation. But inflation returned aggressively in 2021 and remained to form a new inflationary era, with higher interest rates to compensate for lenders for higher inflation. And the huge national debt and national hot air balloon deficits which must be financed by new debt sales, exert increased pressure on long -term rates, including mortgage rates.

These are not normal mortgage rates that are the problem, But prices after absolutely crazy price peaks This results from the QE of the Fed and the repression of interest rates.

Do you like to read Wolf Street and want to support him? You can donate. I really appreciate it. Click on the cup to find out how:

![]()