Unlock the publisher’s digest free

Roula Khalaf, editor -in -chief of the FT, selects her favorite stories in this weekly newsletter.

Do you remember all the speeches of American exceptionalism? The argument that the United States was the only market you needed to worry about, and the major American technology actions were essentially the new risk-free asset?

Well on this subject. . .

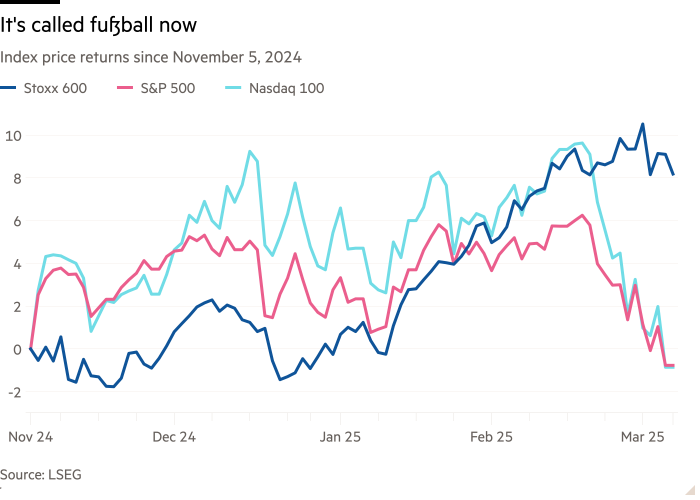

Yes, as many people have noted it happily, European actions have spoken of American actions since the election of Donald Trump. Ok ok, yes, of course, things seem little Different to a longer period – and as the recent oscillation shows, European actions are not entirely safe from all the noise emanating from Washington lately – but it is always a fun development, given the darkness of Europe surrounding and all that “American exceptionalism” chatted last year.

Above all, this seems to arouse real interest in investors, with many analysts on the sales side recently mentioning the number of questions they finally receive on Europe.

And it is now starting to appear in fundflow data. According to the EPFR Global Data, $ 4 billion has flowed in the equity funds in Western Europe on March 5, the most in three years, which brought the entries this year to more than $ 10 billion.

This might seem Dowdy compared to titanic sums which regularly enter funds in American equity and which come out regularly, but it contrasts strongly with the attitude of dominant investors towards Europe in the last decade.

Capital funds in Western Europe have now taken money for four consecutive weeks, the longest entrance sequence since mid-201 Mania.

So how long can it last? Who knows. Europe is essentially the Tottenham Hotspur of the international economy – sometimes promising, sometimes embarrassing, ultimately disappointing and incapable of winning prizes since 2008.

However, there seems to be a provisional but fundamental change in recently vibrations (in European markets, not in northern London).

The European Barclays shares team says that the performance of European stock market markets has so far been mainly a “rescue rally”, but argue that the recent news in Germany could be the spark of a regime change. Alphaville’s accent below:

The outperformance on the actions of the EU in Jan, FEB, was mainly a rescue rally. Systematic investors have closed their short positions on Europe once it had appeared that prices’ damages may not be as bad as they are fearing, while hopes for a ceasefire in Ukraine and stimulation of EPS revisions from weak FX also helped. This led the multiple p / e in the region to go back to fair value levels above the fair value and to relax the Trump risk premium which has accumulated after the American elections. But while rapid money has become bullish, investors in real currency remain skeptical about the catch -up of Europe which extends well given the still low growth canvas in the region. YTD entries so far have not even completely recovered the redemptions observed in the fourth quarter last year.

However, the German tax bazooka this week and the flow of news reforms at the EU could be a change of diet and mark the advent of Europe 2.0. At least, this is what the synchronized thrust of shares, bond yields and the Eurusd suggests. In addition to considerably higher defense expenses, German proposals include a fund of 500 billion euros to spend on infrastructure and reforming debt braking limits. Meanwhile, monetary policy remains supported with the drop rates of the ECB of 25 pb yesterday, although the reflationary budgetary policy can reduce the chances of making more to come.

Bigger, if some of Draghi’s proposals and other growth / supply policy measures become a reality, it could restart the internal growth engine in Europe and Germany, which has been missing from the GFC. Finally, this could increase growth in Europe above the trend, leading investors to strategically rebalance their benefits more to the region and to generate assessments above average. It is something that few people are still positioned, because we have exceptionalism has been the game book in the past two decades.

In other words. . .